If the word “budget” makes you want to close this tab, you’re exactly who this guide is for.

Here’s the truth most personal finance articles won’t admit: budgeting has a terrible reputation because most people teach it wrong. They hand you a 40-row spreadsheet, tell you to track every coffee, and act surprised when you quit three weeks later. That’s not a budgeting problem — that’s a bad system.

The data backs this up. While roughly 86% of Americans claim to have a budget, studies show only about 40% actually stick to it. And as of early 2026, a sobering 69% of Americans report living paycheck to paycheck — a four-year high — while 57% can’t cover a $1,000 emergency expense. The problem isn’t that people don’t want to budget. It’s that they’ve never been shown a method simple enough to actually maintain.

This guide fixes that. You’re going to learn how to budget for beginners using a simple 5-step method that takes about 30 minutes to set up and 10 minutes a week to maintain. No accounting degree. No guilt. No tracking every single latte. Just a clear, repeatable system that tells your money where to go — instead of wondering where it went.

Let’s build your first budget.

Quick Answer: How Do Beginners Start Budgeting?

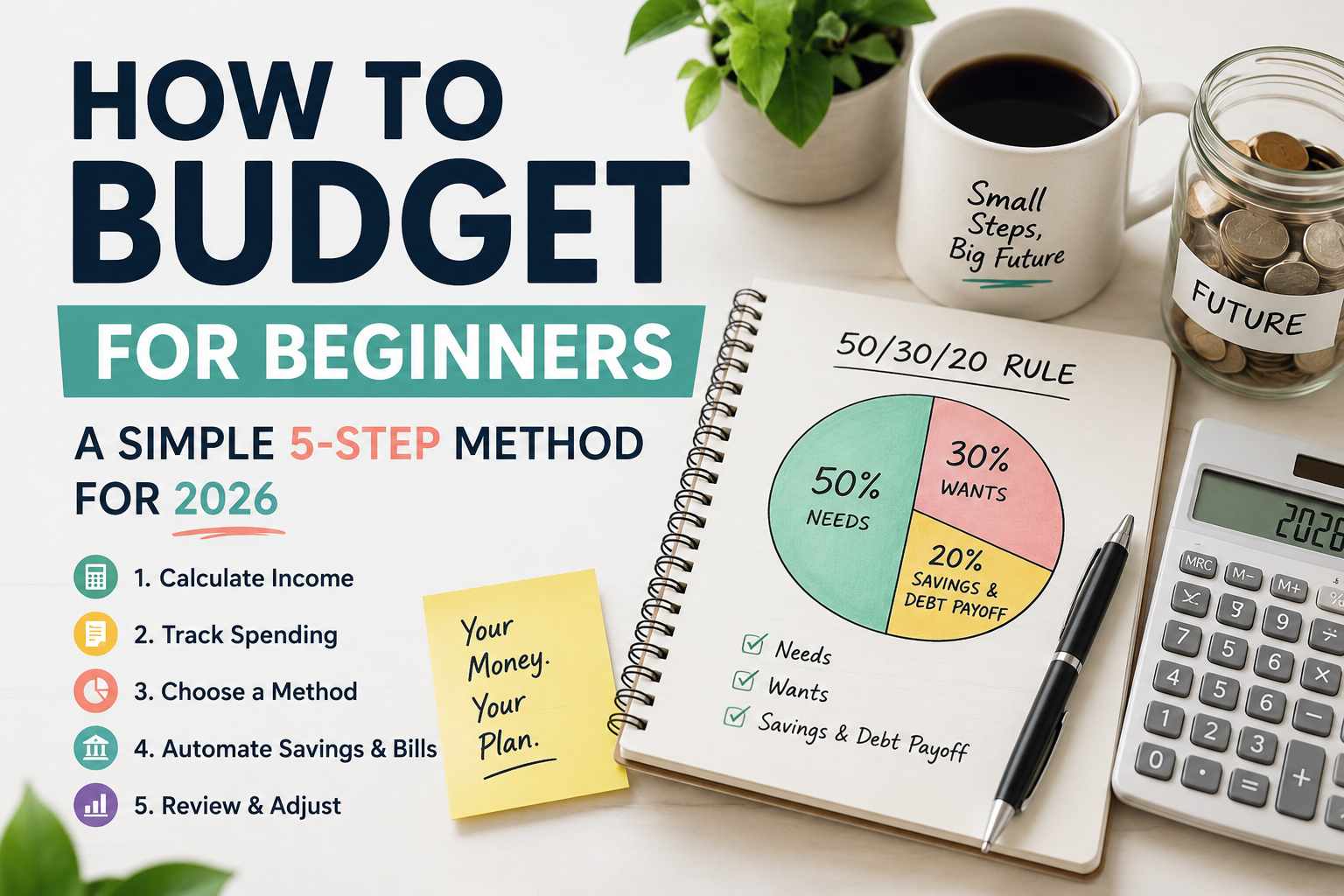

To start budgeting as a beginner, follow these five steps: (1) Calculate your monthly take-home income, (2) Track your current spending for 30 days, (3) Choose a simple budgeting method like 50/30/20, (4) Automate your savings and bills, and (5) Review and adjust monthly. The key to success isn’t perfection — it’s choosing a method simple enough that you’ll actually maintain it. Most beginners see meaningful results within 60–90 days.

Now let’s walk through each step in detail.

Why Budgeting Matters More Than Ever in 2026

Before the how, here’s the why — because motivation matters when you’re starting something new.

Budgeting isn’t about restriction. It’s about control. The research is clear: among Americans who budget consistently, over 84% report it helped them either avoid debt or pay it off. People who track their money are dramatically more financially secure than those who don’t — not because they earn more, but because they direct what they have with intention.

Consider the current landscape: the average American household spent $77,158 in 2024, a 44% increase from a decade earlier. Costs for groceries, housing, and utilities keep climbing. In an environment like this, flying blind with your money isn’t just risky — it’s expensive. A budget is the single most powerful tool you have to fight back against rising costs and build something that lasts.

The best part? You don’t need to be “good with money” to start. You just need a system. Here it is.

Step 1: Calculate Your Real Monthly Income

You can’t divide up money you can’t measure. The foundation of every budget is knowing exactly how much actually lands in your bank account each month.

The key word is take-home pay — your income after taxes, health insurance, and retirement deductions. Not your salary. Not your gross pay. The actual number that hits your account.

Here’s how to find it:

- Salaried, paid biweekly: Look at one paycheck’s deposit amount, then multiply by 2.17 to get your monthly figure (there are 26 paychecks per year, not 24)

- Salaried, paid monthly: Use your single monthly deposit

- Hourly with steady hours: Multiply your average weekly take-home by 4.33

- Irregular or freelance income: Average your last 6 months of deposits, then use the lowest typical month as your baseline (this protects you in lean months)

If you have multiple income sources — a side hustle, partner’s income, child support — add them all together. This combined number is what your entire budget is built on.

Beginner tip: If your income varies a lot, budget based on your lowest recent month. Any extra you earn in good months becomes a bonus you can save or use to pay down debt.

Step 2: Track Your Spending for 30 Days

This is the step most people skip — and it’s the most important one. You cannot build a realistic budget around imaginary numbers. Before you decide where your money should go, you need to see where it actually goes.

For the next 30 days (or by reviewing your last 30 days of statements), categorize every dollar you spent into these buckets:

- Fixed essentials: rent/mortgage, insurance, loan payments, phone

- Variable essentials: groceries, gas, utilities

- Lifestyle/wants: dining out, streaming, shopping, entertainment, hobbies

- Savings/debt payoff: anything you put aside or paid above minimums

You’ll likely have an uncomfortable realization or two. Maybe food delivery added up to $340. Maybe you found subscriptions you forgot existed. This is normal — and it’s the point. The average American spends far more on “wants” than they estimate.

The easiest ways to track:

- Budgeting apps (favored by 27% of young adults): Monarch Money, YNAB, Rocket Money, or your bank’s built-in tools auto-categorize spending

- Spreadsheets (favored by 39% of adults aged 30–44): a free Google Sheet gives you total control

- Pen and paper (still used by many): a simple notebook works if that’s what you’ll stick with

There’s no “right” tool — only the one you’ll actually use. Pick based on your personality, not what an influencer recommends.

Step 3: Choose a Simple Budgeting Method

Now that you know your income (Step 1) and your spending patterns (Step 2), it’s time to give every dollar a job. For beginners, simplicity wins every time. Here are the three best beginner-friendly methods:

The 50/30/20 Rule (Best for Most Beginners)

Split your take-home pay into three buckets:

- 50% to needs — rent, groceries, utilities, minimum debt payments, transportation

- 30% to wants — dining out, entertainment, hobbies, subscriptions

- 20% to savings & debt — emergency fund, retirement, extra debt payments

This is the most popular method because it’s balanced, flexible, and easy to remember. It builds in guilt-free spending money, which is exactly why people stick with it.

Example on a $4,000/month take-home income:

| Category | Percentage | Monthly Amount |

|---|---|---|

| Needs | 50% | $2,000 |

| Wants | 30% | $1,200 |

| Savings & Debt | 20% | $800 |

Zero-Based Budgeting (Best for Detail-Oriented Beginners)

Every dollar gets assigned a specific job until your income minus expenses equals zero. Income – Expenses – Savings = $0. This offers maximum control but requires more tracking.

The Pay-Yourself-First Method (Best for Simplicity)

Decide on a savings amount, automate it immediately when you get paid, and spend the rest however you want. The simplest method of all — ideal if detailed tracking overwhelms you.

For your first budget, I recommend the 50/30/20 rule. It’s the easiest to maintain and gives you a balanced foundation you can refine later.

Step 4: Automate Your Savings and Bills

This is the secret weapon that separates people who succeed at budgeting from people who quit. Willpower is unreliable. Automation is bulletproof.

Here’s what to set up:

1. Automate your savings first (pay yourself first) Set up an automatic transfer from checking to a high-yield savings account (HYSA) for the day after each payday. If your 20% savings target is $400/paycheck, that $400 moves before you can spend it. As of 2026, top HYSAs pay 4.00–4.75% APY versus the national average of about 0.45% — so your emergency fund actually grows.

2. Automate your bills Put every fixed bill on autopay — rent, utilities, insurance, minimum debt payments. This single move prevents late fees and protects your credit score (one missed payment can drop your score by 17–83 points).

3. Split your paycheck at the source (advanced tip) Many employers let you direct-deposit into multiple accounts. Send your savings portion straight to your HYSA before it ever touches checking. You’ll never miss money you never see.

The goal: make the right financial behavior happen automatically, so your budget works even on weeks when you’re busy, tired, or stressed.

Step 5: Review and Adjust Monthly

A budget isn’t a one-time setup — it’s a living system. The final step is a quick monthly review that keeps everything on track.

On the first of each month, spend 15 minutes reviewing:

- Did I hit my targets? Compare actual spending to your planned 50/30/20 split

- Where did I overspend? Identify the one or two categories that ran over

- Any new leaks? Check for subscriptions that crept back or spending creep

- Upcoming irregular expenses? Car registration, holidays, annual fees — plan ahead with a small “sinking fund”

Here’s the critical mindset shift: overspending isn’t failure — it’s data. If you blew your dining budget by $150 in March, that’s not a reason to quit. It’s information that helps you adjust April. The people who succeed at budgeting aren’t perfect; they just keep adjusting and never quit entirely.

Most beginners find their budget starts feeling natural after about three months. The first month is the hardest. By month three, it’s a habit.

Common Beginner Budgeting Mistakes to Avoid

Mistake 1: Being too restrictive. If your budget has zero fun money, you’ll abandon it within weeks. Build in wants — it’s what makes the system sustainable.

Mistake 2: Forgetting irregular expenses. Car repairs, holiday gifts, annual subscriptions — these blow up budgets when ignored. Set aside a small monthly amount in a “sinking fund” to cover them.

Mistake 3: Using gross income instead of take-home. Always budget with your actual after-tax pay, or your numbers will never balance.

Mistake 4: Quitting after one bad month. Progress beats perfection every time. One overspending month doesn’t undo the system.

Mistake 5: Skipping the emergency fund. Before aggressively paying off debt or investing, build a $1,000 starter emergency fund. It prevents new debt when life happens — and life always happens.

Mistake 6: Tracking everything obsessively. You don’t need to log every $2 purchase. Track categories, not pennies. Obsessive tracking leads to burnout.

Frequently Asked Questions

What is the best budgeting method for beginners?

The best budgeting method for beginners is the 50/30/20 rule — splitting take-home pay into 50% needs, 30% wants, and 20% savings. It’s simple, flexible, balanced, and easy to remember, which makes it the most sustainable option for people who are new to budgeting. Detail-oriented beginners may prefer zero-based budgeting, while those who want maximum simplicity can use the pay-yourself-first method.

How much should a beginner budget for savings?

Beginners should aim to save 20% of their take-home income following the 50/30/20 rule. If that’s not realistic at first, start with whatever you can — even $50 per paycheck — and increase it over time. The habit of saving consistently matters more than the exact amount when you’re starting out. Build a $1,000 emergency fund first, then work toward 3–6 months of expenses.

How do I budget if I live paycheck to paycheck?

If you’re living paycheck to paycheck, start by tracking every expense for 30 days to find spending leaks. Focus first on building a small $500–$1,000 emergency buffer, even if it means saving just $25 per week. Then attack the “Big Three” expenses — housing, transportation, and food — since these offer the biggest savings potential. Consider a modified budget like 70/20/10 until your situation improves.

What is the 50/30/20 rule of budgeting?

The 50/30/20 rule is a budgeting method that divides your after-tax income into three categories: 50% for needs (rent, groceries, bills), 30% for wants (dining, entertainment, hobbies), and 20% for savings and debt repayment. It was popularized by Senator Elizabeth Warren and is widely considered the best starting framework for budgeting beginners.

How long does it take for a budget to start working?

Most beginners find their budget starts feeling natural and working effectively after about three months. The first month involves setup and adjustment, the second month refines your category amounts, and by the third month, budgeting becomes a sustainable habit rather than a chore.

Do I need a budgeting app to start?

No. While budgeting apps like Monarch Money, YNAB, and Rocket Money make tracking easier, you can budget perfectly well with a free spreadsheet or even pen and paper. The best tool is the one you’ll actually use consistently. Many successful budgeters use simple methods — what matters is sticking with it, not the technology.

Final Thoughts

Budgeting for beginners comes down to one principle: a budget isn’t a cage — it’s a plan that gives you permission to spend without guilt and save without stress. You’re not restricting your money; you’re directing it toward what actually matters to you.

The 5-step method works because it’s simple enough to maintain: calculate your income, track your spending, pick the 50/30/20 method, automate everything, and review monthly. That’s it. No accounting degree required, no obsessive tracking, no shame.

Here’s your challenge: don’t wait for the perfect moment or the first of the month. Open your banking app right now and complete Step 1 — calculate your real take-home pay. Then schedule 30 minutes this weekend to finish the setup.

In 90 days, you’ll have something most Americans never build: complete clarity about where your money goes, and the confidence that comes with finally being in control. Your future self will thank you for starting today.