Your three-digit credit score quietly runs your financial life. It decides whether you get approved for an apartment, what you pay for car insurance, whether a bank approves your mortgage — and how much that mortgage costs you over the next 30 years.

Here’s the staggering reality most Americans don’t realize: the difference between a “fair” credit score (620) and an “exceptional” one (760+) on a typical $350,000 mortgage adds up to roughly $134,000 in extra interest over the life of the loan. That’s a college education. A down payment on a second home. A decade of retirement savings — all decided by a number most people couldn’t define if you asked them.

So what is a good credit score in 2026? Where do you actually stand? And what does each credit score range unlock or block?

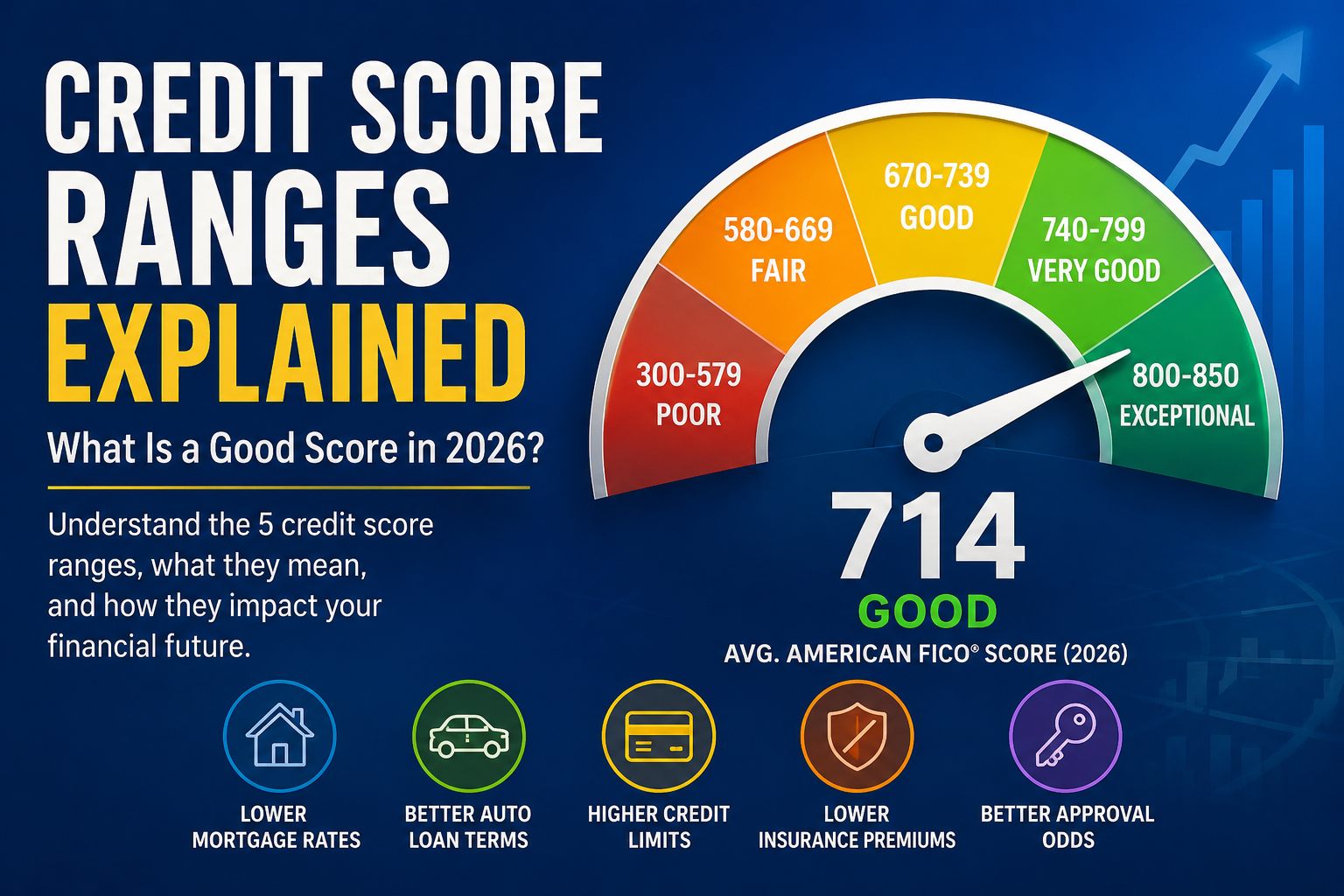

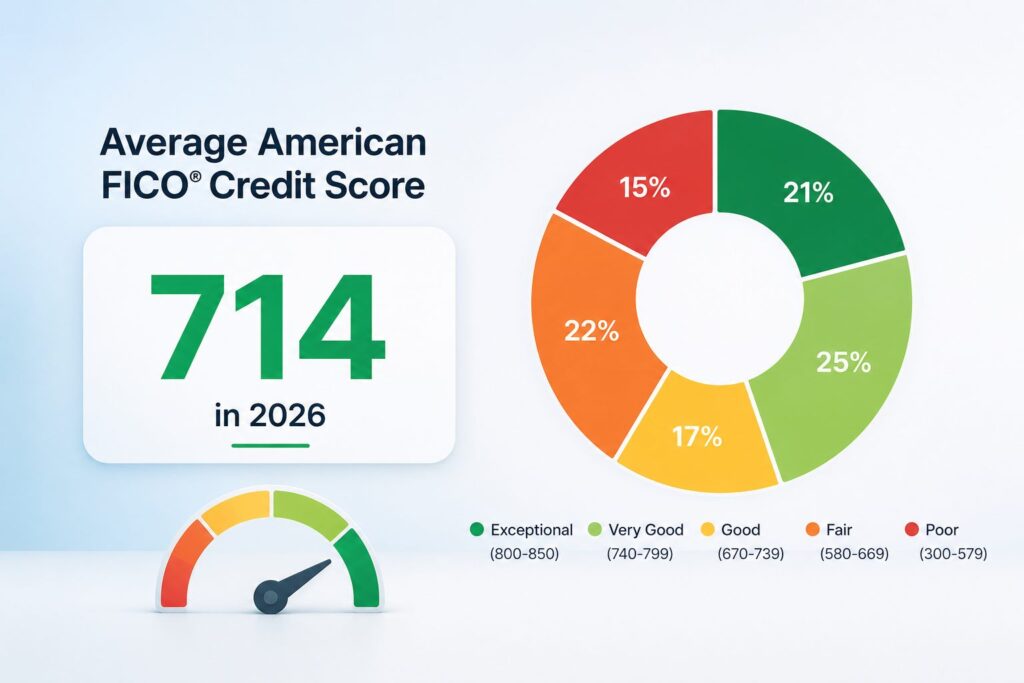

According to the Spring 2026 FICO® Score Credit Insights report, the average American FICO Score is 714 — placing the typical person squarely in the “good” range. But “good” and “great” are separated by thousands of dollars per year in real money. This complete beginner guide breaks down every credit score range, what each one means, what it actually qualifies you for in 2026, and exactly how to push your number higher.

Quick Answer: What Is a Good Credit Score?

A good credit score is generally defined as 670 or higher on the FICO Score scale, which ranges from 300 to 850. As of 2026, the average American FICO Score is 714, with approximately 71% of Americans holding a score of 670 or above. While 670 qualifies as “good,” lenders typically reserve their best interest rates for borrowers scoring 740 or higher — and the most premium pricing for those at 760 and above.

Now let’s break down each range in detail.

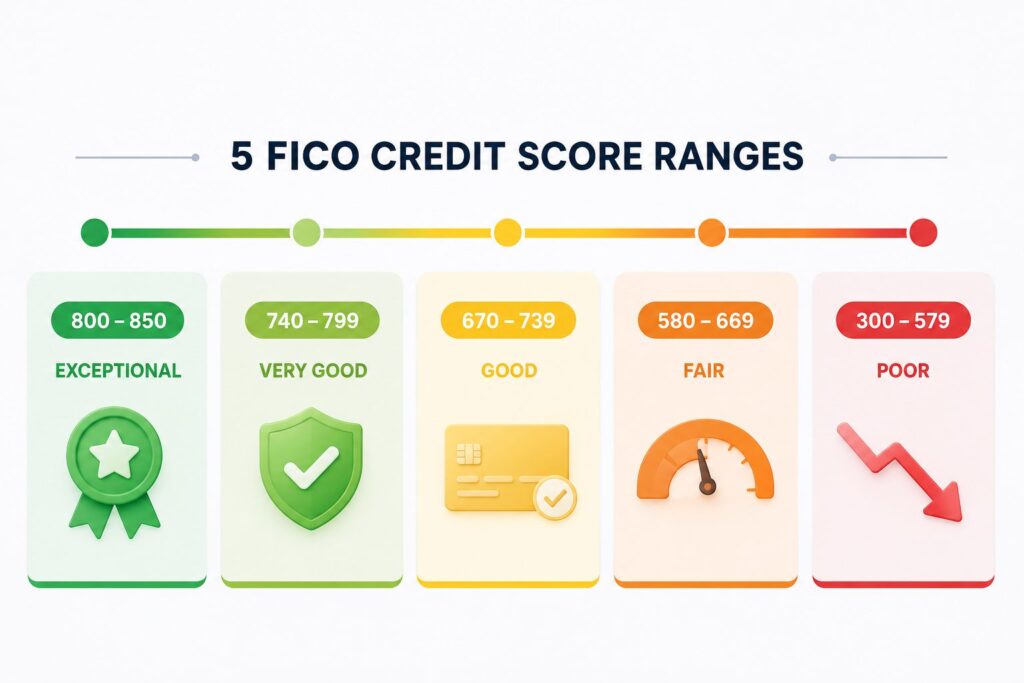

The 5 FICO Credit Score Ranges (2026)

FICO Scores — used by approximately 90% of top US lenders — are divided into five categories. Each tier unlocks different rates, products, and approval odds.

| Score Range | Tier | % of Americans (2026) |

|---|---|---|

| 800–850 | Exceptional | ~24% |

| 740–799 | Very Good | ~24% |

| 670–739 | Good | ~23% |

| 580–669 | Fair | ~13% |

| 300–579 | Poor | ~16% |

Almost half of all US consumers (48.1%) now have a FICO Score of 750 or higher — a record-breaking statistic that reflects what FICO calls a “K-shaped economy,” where high-score and low-score segments are both growing while the middle shrinks.

Let’s break down what each tier actually means for your wallet.

Check Previous Blog: 5 Credit Card Mistakes That Cost You Thousands

Exceptional Credit (800–850)

Roughly 24% of Americans fall into this top tier, though fewer than 2% reach the maximum score of 850.

What it unlocks:

- Access to virtually any credit product on the market

- The lowest possible interest rates on mortgages, auto loans, and personal loans

- Premium rewards credit cards (Chase Sapphire Reserve, Amex Platinum, etc.)

- Highest credit limits — often $30,000+ per card

- The best balance transfer and 0% intro APR offers

- Lowest auto insurance premiums in most states

- Easier approval for rental properties and apartments

Real-world example: On a $350,000 30-year mortgage, a borrower with an 800 score might secure a rate around 6.15% APR — saving roughly $134,000 in interest over the loan’s life compared to a fair-credit borrower at 7.72%.

Very Good Credit (740–799)

Another 24% of Americans sit in this range — the sweet spot for most premium financial products.

What it unlocks:

- Below-average interest rates on most loans

- Approval for nearly all major rewards credit cards

- Strong negotiating position with lenders

- Better rental and insurance terms

- Access to 0% intro APR balance transfer cards with the longest terms (15–21 months)

The difference between “very good” and “exceptional” is usually only a few basis points on most loans — but it matters more on large mortgages where every 0.25% adds up to thousands.

Good Credit (670–739)

This is the national average tier, holding about 23% of consumers. The current US average of 714 falls right in this range.

What it unlocks:

- Approval for most standard credit cards and loans

- Reasonable but not premium interest rates

- Most lenders consider you a “low-risk” borrower

- Decent credit card limits ($5,000–$15,000 typically)

- Mortgage approval, but not at top-tier rates

The catch: A 670 score is technically “good,” but lenders often reserve their best pricing for 740+. If you’re at 700, you’re still paying a meaningful premium on most loans compared to someone at 760.

Real-world example: On the same $350,000 mortgage, a borrower with a 700–720 score might pay roughly 6.63% APR — about $107/month more than a borrower at 760, or $38,500+ more over 30 years.

Fair Credit (580–669)

About 13% of Americans are in the fair range. This is the tier where borrowing starts to get expensive — and approval starts to get harder.

What it unlocks (and what it doesn’t):

- Approval for some credit cards, but usually with higher APRs (24–28%)

- Auto loans available, but at significantly higher rates (10–15%)

- Mortgage approval is possible but with higher rates and stricter terms

- Many premium rewards cards and 0% APR offers are out of reach

- Higher insurance premiums in most states

- Apartment rentals may require larger security deposits

This is the tier where small improvements pay off most. Moving from 640 to 690 can shift you into a completely different pricing bracket on auto and home loans — often saving $50–$200 per month.

Check Previous Blog: 50/30/20 Budget Rule Explained

Poor Credit (300–579)

Approximately 16% of Americans fall into the poor credit range — a number that has grown in 2026 as student loan delinquencies returned to credit reports.

What it looks like:

- Most traditional credit cards will deny applications

- Auto loans are available but at subprime rates (15–25% APR)

- Mortgages are usually only available through FHA programs with strict requirements

- Secured credit cards (requiring a deposit) become the primary credit-building tool

- Higher utility and phone deposits often required

- Some employers may check credit for finance-related positions

The good news: Poor credit is the most fixable. With consistent on-time payments and low utilization, scores in this range often jump 50–100 points within 12 months of focused effort.

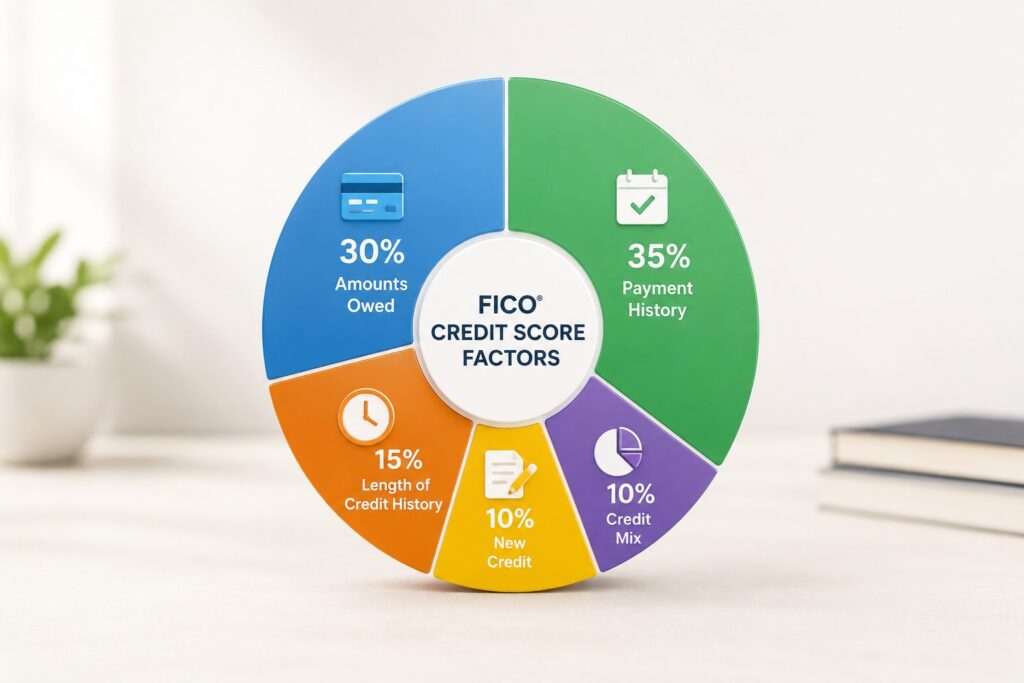

How FICO Calculates Your Score (The 5 Factors)

Your FICO Score is built from five weighted factors. Understanding them is the foundation of improving your number.

1. Payment History (35%) — The Biggest Factor

Whether you’ve paid your past credit accounts on time. This is the single largest contributor to your score.

- One 30-day late payment can drop a 780 score by 60–100 points

- A 90-day late payment can hit even harder, dropping scores by 100–150+ points

- Late payments stay on your credit report for 7 years, though their impact fades over time

- Recent late payments hurt much more than older ones

Action step: Set up autopay for at least the minimum on every account. This single move prevents the most damaging score drops.

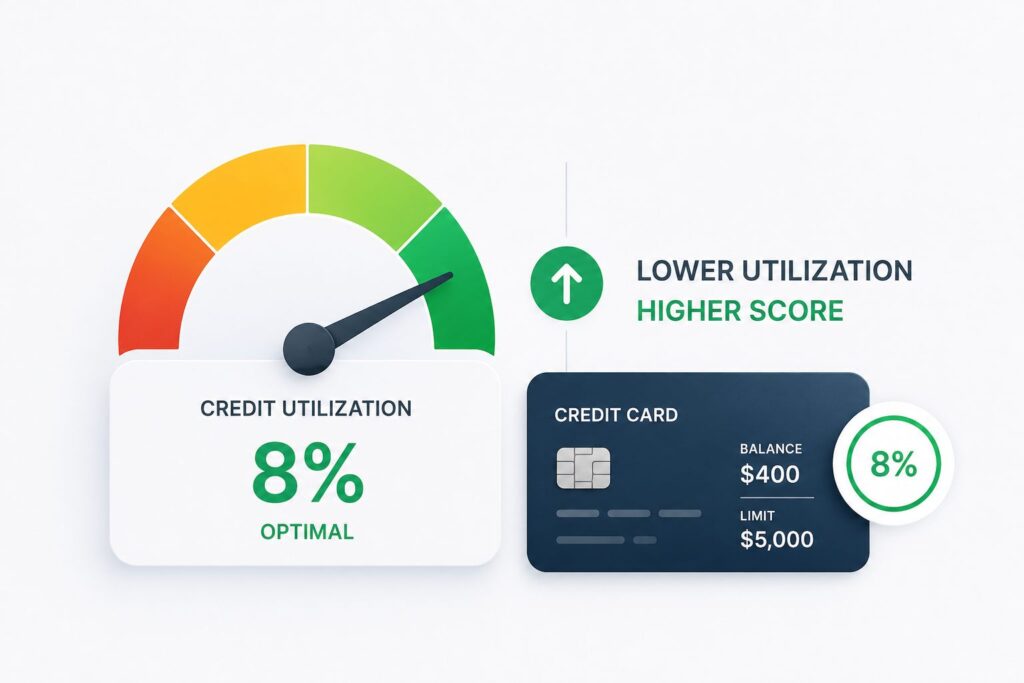

2. Amounts Owed / Credit Utilization (30%)

The total amount of credit you’re using compared to your total credit limit. If you have $10,000 in total credit limits and $3,000 in balances, your utilization is 30%.

Key benchmarks in 2026:

- Under 10% utilization: Optimal — scores in the 800s typically maintain this

- 10–30%: Generally good — most experts recommend staying under 30%

- 30–50%: Begins hurting your score noticeably

- Over 50%: Major negative impact

- Over 75% or maxed out: Severe damage

According to recent data, the average US utilization rate jumped to 36.1% in early 2026 — well above the recommended threshold and contributing to the national score decline.

Action step: Pay down balances before your statement closes, not just before the due date. The balance reported to credit bureaus is usually your statement balance — paying early lowers what gets reported.

3. Length of Credit History (15%)

How long you’ve had credit. This includes the age of your oldest account, your newest account, and the average age across all accounts.

Why this matters: Lenders trust borrowers with proven track records. A 20-year-old account in good standing carries enormous weight.

Action step: Never close your oldest credit card if it has no annual fee. Closing it shortens your history and reduces your available credit — a double hit.

4. New Credit (10%)

How often you apply for new accounts. Each application creates a hard inquiry, which can drop your score 5–10 points.

- Multiple applications in a short window signal financial distress to lenders

- Hard inquiries stay on your report for 2 years (but only affect your score for 12 months)

- Rate-shopping exception: Multiple mortgage or auto loan inquiries within a 14–45 day window count as a single inquiry

Action step: Don’t apply for new credit within 6 months of a major loan application like a mortgage.

5. Credit Mix (10%)

The variety of credit products you have — credit cards, installment loans, auto loans, mortgages. Lenders prefer borrowers who can handle multiple types of credit responsibly.

Action step: Don’t open new accounts just for variety — but if you only have credit cards, adding a small installment loan (like a credit-builder loan) over time can help.

FICO vs. VantageScore: What’s the Difference?

You’ll see two main credit scoring models in 2026:

FICO Score

- Used by approximately 90% of top US lenders

- Range: 300–850

- Required for most mortgages, auto loans, and credit cards

- Most authoritative score

VantageScore

- Developed jointly by Experian, TransUnion, and Equifax

- Same 300–850 range

- Used by Credit Karma, Credit Sesame, and many bank dashboards

- Free monitoring services typically show this

- Slightly different calculation — can score 20–40 points higher or lower than FICO

The takeaway: Free apps like Credit Karma show your VantageScore — useful for tracking trends but not what most lenders see. When applying for major loans, ask which scoring model the lender uses.

How to Check Your Credit Score for Free in 2026

You have multiple legitimate free options. Checking your own credit (a “soft inquiry”) never hurts your score.

For your credit report (all 3 bureaus):

- AnnualCreditReport.com — The only federally mandated source. The CFPB made weekly free access permanent in 2023.

For your actual credit score:

- Credit Karma — Free VantageScore from TransUnion and Equifax, updated weekly

- Experian — Free FICO Score 8 from Experian

- Your bank or credit card issuer — Most major banks (Chase, Discover, Capital One, Citi, Wells Fargo) provide free FICO scores in their apps

- myFICO.com — Paid service that shows multiple FICO versions used by different lenders

What Hurts Your Credit Score the Most?

Based on 2026 FICO data, the most damaging actions are:

- A bankruptcy — Can drop scores 130–240 points; stays for 7–10 years

- A foreclosure — Drops scores 100–160 points; stays for 7 years

- A 90-day late payment — Drops scores 100–133 points

- A debt sent to collections — Drops scores 50–100 points

- A 30-day late payment — Drops scores 17–83 points

- Maxing out a credit card — Can drop scores 10–45 points

- A hard inquiry — Drops scores 5–10 points

- Closing an old credit card — Variable impact, can drop scores 10–30 points

How to Improve Your Credit Score Fast

For most Americans, focused effort over 3–6 months can move scores by 30–80 points. Here’s the priority order:

- Pay every bill on time — even one late payment can erase months of progress

- Pay down credit card balances to below 30% utilization (ideally under 10%)

- Don’t close old credit cards — keep them open with small recurring charges

- Dispute errors on your credit reports — bureau reporting errors are surprisingly common

- Limit new credit applications to one every 6 months

- Become an authorized user on a family member’s old account in good standing

- Consider a secured credit card if you have limited or damaged credit history

Frequently Asked Questions

What is considered a good credit score in 2026?

A good credit score in 2026 is 670 or higher on the FICO scale. The current US average is 714, which falls in the “good” range. However, lenders typically reserve their best interest rates for borrowers with scores of 740 or higher (very good) and the absolute best pricing for 760+ (exceptional).

What is the average credit score in America?

According to the Spring 2026 FICO Score Credit Insights report, the average American FICO Score is 714 — down 2 points from the previous year, primarily due to resumed student loan delinquency reporting after the multi-year pandemic pause.

Why did my credit score drop suddenly?

Sudden score drops are usually caused by one of these factors: a late payment being reported, a major increase in credit utilization, a new hard inquiry, an account closure, or a collection account appearing on your report. In 2026 specifically, over 2 million borrowers experienced 100+ point drops due to student loan delinquencies returning to credit reports.

How long does it take to build good credit?

For someone starting from scratch, it takes about 6 months to generate a FICO Score and roughly 12–24 months of responsible credit use to reach the “good” range (670+). Reaching “exceptional” (800+) typically requires 5+ years of consistent on-time payments and low utilization.

Does checking my own credit score hurt it?

No. Checking your own credit score is a “soft inquiry” and has zero impact on your credit. You can check your score as often as you want without consequences. Only “hard inquiries” — when a lender pulls your credit during a loan or credit card application — can affect your score.

What’s the difference between a credit score and a credit report?

Your credit report is the underlying record of your credit history — all your accounts, payments, balances, and inquiries. Your credit score is a three-digit number calculated from the data in your credit report. Reports are maintained by the three major bureaus (Experian, TransUnion, Equifax); scores are calculated by FICO or VantageScore using the report data.

Final Thoughts

Your credit score isn’t just a number — it’s the most consequential financial credential most Americans will ever own. The difference between a fair score and an exceptional one isn’t theoretical. It’s the difference between getting approved or denied, between paying $2,100 a month on a mortgage or $2,500, between affordable car insurance and overpriced premiums.

The good news? Every range on this scale is reachable with consistent effort. The single biggest predictor of where you’ll be in 12 months isn’t your current score — it’s whether you pay every bill on time and keep your utilization low. That’s it. Two habits, repeated month after month, move people from fair to good, from good to very good, from very good to exceptional.

Check your score this week. Note your current range. Apply the priority list above. In 6 months, you’ll likely be one tier higher — and you’ll feel the difference everywhere money touches your life.