Most Americans aren’t broke because they don’t earn enough. They’re broke because of five small credit card habits that quietly siphon thousands of dollars out of their bank accounts every year — often without them noticing.

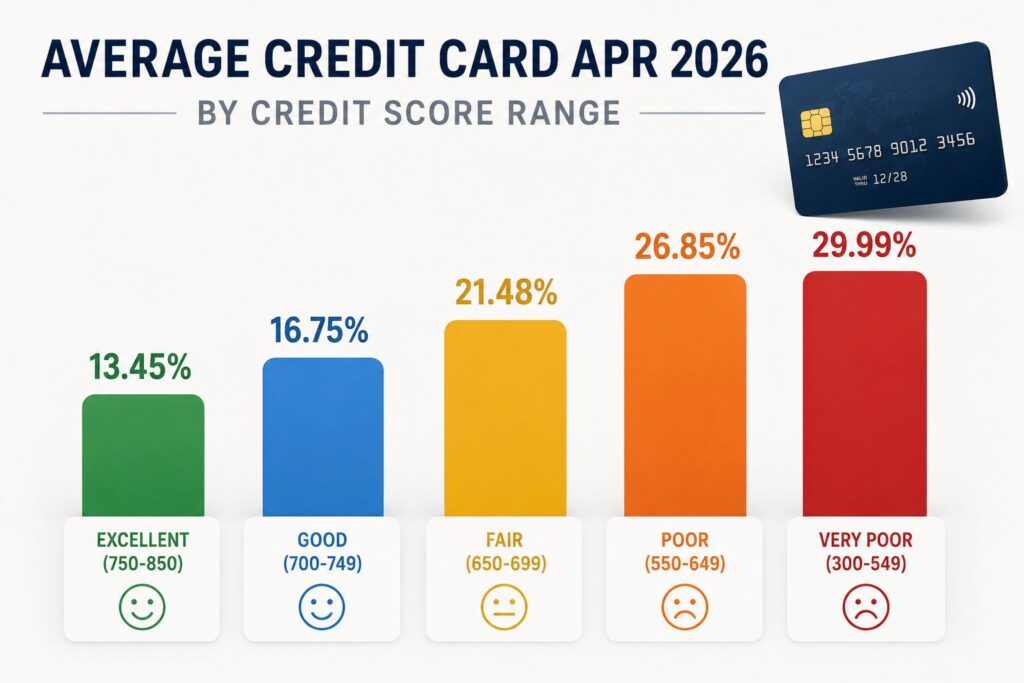

Here’s the math that should scare you: Americans collectively owe $1.252 trillion in credit card debt as of Q1 2026, according to the Federal Reserve. The average household carries $9,474 in revolving balances, paying an average APR of 21.52% on accounts accruing interest, with new card offers averaging 23.75%. For every day this country doesn’t have a credit card rate cap, consumers accrue approximately $368 million in interest — straight to the banks.

That’s not bad luck. That’s a system designed to profit from common credit card mistakes. The good news? Every mistake in this guide is 100% fixable, often in a single afternoon.

If you’ve ever wondered why your balance never seems to go down despite making payments, you’re probably making at least three of these five mistakes right now. Let’s break them down — and exactly what each one costs you.

Quick Answer: What Are the Most Expensive Credit Card Mistakes?

The five most expensive credit card mistakes Americans make in 2026 are: (1) paying only the minimum balance, (2) taking cash advances, (3) missing payments and triggering penalty APRs, (4) carrying a balance on rewards cards, and (5) ignoring foreign transaction and balance transfer fees. Together, these mistakes cost the average cardholder $1,500–$9,000+ over the life of their debt. Fixing them is the single highest-return financial habit available to most Americans.

Now let’s break down each one in detail — with real 2026 cost numbers.

1. Paying Only the Minimum Balance

What it costs you: $5,000–$9,000+ in lifetime interest on a $6,500 balance How long it traps you in debt: 18+ years

This is the single most expensive credit card mistake in America — and the one that affects the most people. Most credit card issuers set the minimum payment at just 2–3% of your balance. It feels manageable. It looks responsible. It’s a financial trap.

Here’s the actual math, based on 2026 Federal Reserve data: a cardholder carrying the average $6,500 balance at 22.4% APR, making only minimum payments, will take over 18 years to pay off the balance — and will pay more than $9,000 in interest alone in the process. That’s more than the original debt itself.

Why does this happen? Because of how compound interest works. When you pay only the minimum:

- Most of your payment goes to interest, not principal

- The remaining principal continues to accrue interest at 20%+

- Your balance barely moves month to month

- You stay in debt for decades — by design

Real example:

| Strategy | Time to Pay Off $6,500 | Total Interest Paid |

|---|---|---|

| Minimum payment only (~$130/month) | 18+ years | $9,000+ |

| $250/month fixed payment | 3 years | $2,200 |

| $400/month fixed payment | 1.6 years | $1,100 |

| Pay in full each month | 0 months | $0 |

The fix: Pay your full statement balance every month. If you can’t, pay at least 3x the minimum to make meaningful progress. Even better, switch to weekly payments instead of monthly — this lowers your average daily balance, which is what interest is calculated on.

2. Taking Cash Advances

What it costs you: $80–$300+ in immediate fees and interest on a single $1,000 advance Effective APR: Often 27–35%, with NO grace period

A cash advance is the most expensive way to borrow money from a credit card — and millions of Americans use them without understanding what they’re actually paying.

Here’s what happens the moment you take a $1,000 cash advance:

- Cash advance fee: Typically 5% of the amount, or roughly $50 (minimum $10)

- ATM fee: $2–$5 if you use an out-of-network ATM

- Higher APR: Cash advance APRs are usually 25–29%, vs. ~22% for purchases

- No grace period: Interest starts accruing the moment you take the cash — not after 21 days like regular purchases

- Payment priority: Under Regulation Z, if you only make the minimum payment, the issuer can apply most of it to your lower-APR purchases first, letting the cash advance keep compounding

Even worse: cash advances can hurt you in ways most people don’t realize. Credit card companies may view repeated cash advances as a sign of financial distress. This can trigger a rate increase on your entire account, lower your credit limit, or in extreme cases, lead to account closure.

Real example: A $1,000 cash advance at 27% APR carried for 30 days costs:

- $50 cash advance fee

- ~$22 in interest (accrued daily from day one)

- $3 ATM fee

- Total: $75 to borrow $1,000 for one month — an effective annual rate of ~90%

The fix:

- For emergencies: a personal loan from a credit union, even at 14–18% APR, is dramatically cheaper

- Ask creditors for hardship extensions before resorting to cash advances

- Some employers offer earned-wage access (much cheaper than payday alternatives)

- If you must take an advance, pay it off immediately — every day adds compounding interest

3. Missing Payments and Triggering Penalty APRs

What it costs you: Up to $300+ per missed payment, plus long-term credit score damage Credit score impact: Drops of 17–133 points

Most cardholders know late fees exist. Few understand the full cascade of consequences from a single missed payment in 2026.

Here’s the full price tag of one late payment:

- Late fee: Up to $30 for first offense, $40 for repeat offenses within six billing cycles

- Penalty APR: Some issuers can raise your APR to 29.99% on the entire balance — sometimes permanently

- Credit score damage: Once a payment is 30 days past due, it gets reported to credit bureaus. According to FICO data, this can drop your score by 17–83 points. At 90 days, the drop can hit 133 points.

- Future borrowing cost: A damaged credit score means higher rates on mortgages, auto loans, insurance premiums, and even apartment applications — potentially tens of thousands of dollars over your lifetime

- Grace period loss: Once you miss a payment, many cards revoke your interest-free grace period on new purchases

Real example: A single 90-day late payment on a $5,000 balance with a 22% APR can trigger:

- $40 late fee

- A penalty APR jump to 29.99% (adds ~$33/month extra interest)

- A credit score drop of 100+ points

- A 0.5–1% higher rate on your next mortgage (could cost $50,000+ over 30 years on a $300K mortgage)

The fix:

- Set up autopay for at least the minimum payment on every card you own (this single move prevents 95% of late payments)

- Add a backup calendar reminder 3 days before due dates

- If you’ve never been late before, call your issuer immediately after a missed payment — most will waive the first late fee on request

- After 6 months of perfect payments, request that the penalty APR be removed

4. Carrying a Balance on a Rewards Card

What it costs you: Often 10x more than you earn in rewards Why it’s worse than a regular card: Higher APRs

This mistake is especially insidious because it disguises itself as smart financial behavior. People sign up for cashback or travel rewards cards thinking they’re “winning” — then carry a balance and quietly lose far more than they earn.

The math is brutal. A typical 2% cashback card pays you $20 in rewards on $1,000 spent. But if you carry that $1,000 balance for a year at 24% APR (rewards cards often have higher APRs than basic cards):

- Rewards earned: $20

- Interest paid: ~$240

- Net loss: -$220

You’re paying 12x what you’re earning. Every “free” trip or cashback bonus you’ve ever celebrated is wiped out — and then some — the moment you stop paying in full.

Worse, the psychological effect of rewards cards encourages spending. Multiple consumer studies have shown that cardholders spend 10–30% more on rewards cards than they would with cash or debit, because the “earning rewards” mindset reduces the pain of payment.

Real example: A traveler racks up $50,000 in spending over a year on a 2x miles card. Sounds great — 100,000 miles, potentially worth $1,500–$2,000 in flights. But if they carried even a $5,000 average balance throughout the year at 24% APR, they paid roughly $1,200 in interest. The “reward” is essentially canceled out, and the cardholder is now $5,000 in debt.

Check Our Previous Blog: 50/30/20 Budget Rule Explained: Complete Beginner Guide

The fix:

- Two-card strategy: Use a low-APR card (or 0% intro APR card) for any balances you carry, and a rewards card ONLY for purchases you can pay in full

- If you currently carry a balance on a rewards card, transfer it to a 0% intro APR balance transfer card immediately

- Never apply for a rewards card if you’re not 100% confident you can pay in full every month

- Treat rewards as a bonus on responsible spending, not as a justification for new spending

5. Ignoring Foreign Transaction, Annual, and Balance Transfer Fees

What it costs you: $100–$600+ per year in avoidable fees Most common silent drain: Foreign transaction fees

This is the “death by a thousand cuts” mistake. Each individual fee feels small. Stacked together over years, they’re one of the largest drains on the average cardholder’s wallet.

The most common fees Americans pay without realizing:

Foreign transaction fees: Typically 3% per transaction. If you spend $3,000 abroad on vacation, that’s $90 in pure fees — even if you pay your balance in full. Many premium travel cards have zero foreign transaction fees, but most basic cards charge them.

Annual fees: $95–$695. Premium cards charge annual fees that only make sense if you actively use the benefits. A $550 annual fee card with travel credits, lounge access, and statement credits can be worth it for frequent travelers — but if you barely fly, you’re paying $550 for marketing you ignore.

Balance transfer fees: 3–5% of the transferred amount. Often worth paying if it gets you a 0% APR period, but only if you have a clear plan to pay off the balance before the intro period expires. Otherwise, you’re paying a fee AND paying interest later.

Over-limit fees: Mostly banned by the CARD Act of 2009, but can still apply if you opt in. Never opt in.

Returned payment fees: Up to $40 if your autopay bounces. Make sure your linked account always has sufficient funds.

Real example: An American family who traveled to Europe twice in 2026 and used a card with 3% foreign transaction fees on $8,000 of vacation spending paid $240 in fees — money that could have been completely avoided with the right card.

The fix:

- Get one no-foreign-transaction-fee card for travel (many no-annual-fee cards offer this)

- Audit your annual fees yearly — are you actually using the benefits?

- Only transfer balances when you have a real payoff plan before the intro APR expires

- Set up balance and payment alerts via your card’s app to catch problems early

- Call your issuer once a year and ask: “Are any of my fees waivable?” — many will say yes, especially on annual fees

How These 5 Mistakes Stack Up: The Real Cost

Let’s add up what these mistakes cost the average American household over five years:

| Mistake | 5-Year Cost |

|---|---|

| Minimum payments on $6,500 balance | $5,400+ in interest |

| Two cash advances per year ($500 each) | $750 in fees + interest |

| One missed payment with penalty APR | $300 fees + $1,200+ in extra interest |

| Carrying balance on rewards card | $1,000+ net loss vs. rewards earned |

| Annual + foreign transaction fees | $500–$1,500 |

| Total 5-year cost | $9,000–$15,000+ |

That’s the down payment on a house. A year of college. A fully-funded emergency fund. All quietly drained by five fixable habits.

Frequently Asked Questions

What is the most common credit card mistake?

The most common credit card mistake is paying only the minimum monthly payment, which 22% of Americans believe will improve their credit score (it actually hurts it). According to Bankrate’s 2026 survey, 53% of Gen Xers and Millennials carry a balance month-to-month, with 60% having held that debt for at least a year.

Does carrying a balance improve my credit score?

No — this is one of the most damaging myths in personal finance. Carrying a balance hurts your credit score by increasing your credit utilization ratio, and it costs you significant money in interest. To build credit, you only need to use the card and pay it off in full. The balance does not need to remain.

How much does one late credit card payment really cost?

A single late credit card payment can cost between $40 and $300 in immediate fees and penalty interest, plus a credit score drop of 17–133 points depending on how late it is. The long-term cost can be much higher if a damaged credit score raises your future borrowing costs on mortgages, auto loans, or insurance.

Are cash advances ever worth it?

Almost never. With fees averaging 5%, interest rates often above 27%, and no grace period, cash advances are typically the most expensive way to borrow money — often costing the equivalent of a 90–100%+ effective annual rate. Personal loans, credit union loans, or even asking a creditor for a hardship extension are almost always cheaper.

How do I get out of credit card debt fast?

The fastest paths out of credit card debt in 2026 are: (1) transfer balances to a 0% intro APR card (typically 15–21 months interest-free), (2) take out a personal loan at a lower fixed rate (often 12–15% vs. 22%+ on cards), or (3) use the debt avalanche method — pay minimums on all cards but throw everything extra at the highest-APR balance first.

What’s the difference between APR and APY?

APR (Annual Percentage Rate) is the yearly interest rate charged on borrowed money — what you pay on credit card debt. APY (Annual Percentage Yield) is what you earn on savings, factoring in compounding. For credit cards, you care about APR; for high-yield savings accounts, you care about APY.

Final Thoughts

Credit cards aren’t the enemy. Used correctly, they build credit, earn meaningful rewards, and provide stronger fraud protection than debit cards. Used carelessly, they’re the single most expensive financial product the average American household interacts with.

The five mistakes in this guide — minimum payments, cash advances, late payments, balance-carrying on rewards cards, and ignored fees — are the difference between credit cards working for you and silently working against you. Fix even two or three of them and you’ll likely save more money in a year than most people save by cutting subscriptions, switching grocery stores, and clipping coupons combined.

Pull up your statements this week. Find which mistakes you’re making. Fix the easiest one first — usually setting up autopay or moving to twice-monthly payments. Then tackle the next.

The money you save isn’t going to a bank anymore. It’s going to you.