If you’ve ever stared at your paycheck and wondered, “Where does it all go?” — you’re not alone. Most Americans have no formal budget. The ones who try usually quit within 90 days because traditional budgeting feels like accounting homework.

The 50/30/20 budget rule is the antidote. It’s the most popular beginner budgeting framework in the United States for one reason: it works without spreadsheets, willpower marathons, or guilt. You just split your take-home pay three ways and live your life.

But here’s what most articles won’t tell you: the rule was created in 2005, and 2026 looks very different. Rent has outpaced wages in most US metros, grocery prices remain elevated, and student loan payments have restarted. In some cities, “needs” alone eat 60% of income before anything else.

So does the 50/30/20 rule still work? Yes — but with smart modifications. This complete beginner guide breaks down exactly how the rule works, who it’s for, where to adjust it, and how to start using it with your next paycheck.

Quick Answer: What Is the 50/30/20 Budget Rule?

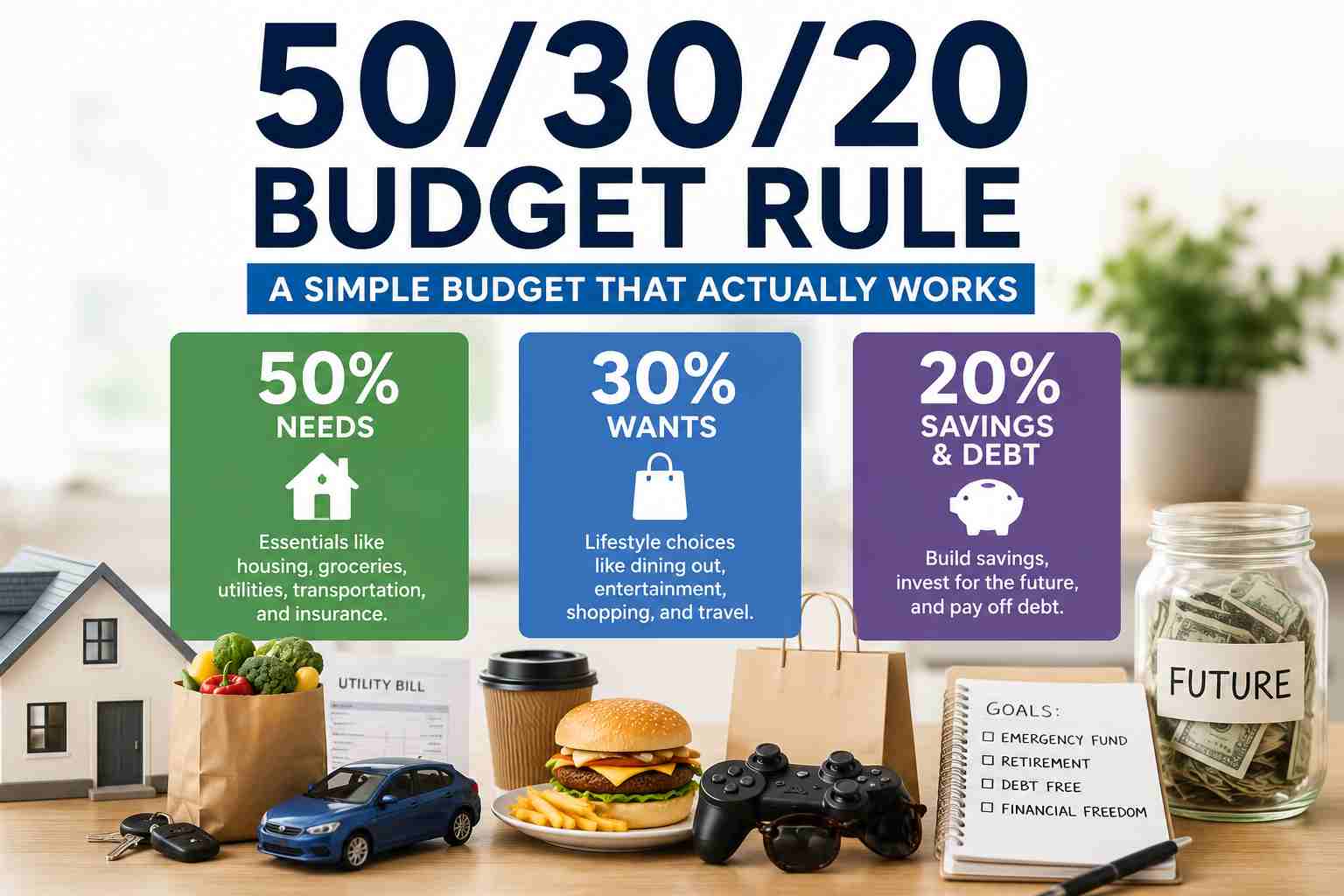

The 50/30/20 budget rule is a simple personal finance framework that divides your after-tax (take-home) income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It was popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in the 2005 book All Your Worth: The Ultimate Lifetime Money Plan. The rule is designed to be simple enough that anyone can follow it without tracking every transaction.

Now let’s break down each piece in plain English.

The 50% Needs Category: Non-Negotiables

The first half of your take-home pay covers expenses you genuinely cannot avoid. If you stopped paying these, your life would meaningfully break — eviction, losing a job, going hungry.

What counts as a need:

- Rent or mortgage payment

- Utilities (electricity, gas, water, basic internet)

- Groceries (not restaurant meals)

- Transportation to work (car payment, insurance, gas, or transit pass)

- Health insurance premiums and essential medications

- Minimum debt payments (credit cards, student loans, personal loans)

- Childcare required for work

- Basic phone plan

- Insurance you legally need (auto, renters, health)

What doesn’t count as a need (even though it feels like one):

- Premium streaming services

- A new car payment when your old car still works

- Brand-name groceries when generics work

- The $90/month phone plan when a $25 plan covers your usage

- Eating out, even cheap takeout

The test: If I lost my income tomorrow, would I still pay this to survive? If yes, it’s a need. If no, it’s a want.

The 30% Wants Category: Lifestyle Money

This is the category most people get wrong — and it’s where the 50/30/20 rule gets its emotional appeal.

The “wants” bucket is everything that improves your quality of life but isn’t strictly necessary. Critically, this 30% is not optional in the philosophy of the rule. Warren’s research showed that budgets without room for enjoyment collapse within months. You need lifestyle money to sustain the system.

What belongs in wants:

- Dining out, takeout, food delivery

- Streaming services (Netflix, Spotify, Disney+, etc.)

- Gym memberships and fitness apps

- Hobbies, books, video games

- Vacations and travel

- Shopping for non-essential clothing

- Upgrades beyond basic (faster internet, premium phone plans, nicer car)

- Concerts, sports tickets, entertainment

- Cosmetics and grooming beyond basics

Pro tip: Subscription bloat lives in this category. The average American spends $219/month on subscriptions but estimates only $86. Auditing this bucket quarterly typically frees up $80–$150/month — money that can shift directly to your 20% savings goal.

The 20% Savings & Debt Category: Future You

This is the most important 20% of any paycheck. It’s also the one most people sacrifice first when money gets tight — and regret most by retirement.

What belongs here:

- Emergency fund contributions (target: 3–6 months of expenses)

- Retirement accounts (401(k) contributions, IRA, Roth IRA)

- Brokerage investments

- Extra debt payments above the minimum (the minimum goes in “needs”)

- Down payment savings (house, car)

- Major goal savings (wedding, business launch, education)

The order of priority matters when your 20% is limited:

- Build a $1,000 starter emergency fund first — this prevents new credit card debt during emergencies

- Pay off any debt above 8% interest (most credit cards qualify)

- Capture full employer 401(k) match — it’s free money, often a 50–100% instant return

- Build emergency fund to 3–6 months of expenses

- Max out tax-advantaged accounts (Roth IRA, 401(k))

- Invest in taxable brokerage for medium-term goals

How to Apply the 50/30/20 Rule: A Real Example

Let’s walk through this with a real US income.

The median US household income in 2024 was $83,730, according to the US Census Bureau, and projections for 2026 put the figure between $89,000 and $90,000. After federal income tax, FICA (Social Security + Medicare), and average state tax, take-home pay on a $90,000 household income is roughly $70,000/year — or about $5,830/month.

Here’s what the 50/30/20 split looks like at that income:

| Category | Percentage | Monthly Amount |

|---|---|---|

| Needs | 50% | $2,915 |

| Wants | 30% | $1,749 |

| Savings & Debt | 20% | $1,166 |

| Total | 100% | $5,830 |

Now, a realistic breakdown of those buckets:

Needs ($2,915/month):

- Rent or mortgage: $1,500

- Utilities & internet: $250

- Groceries: $500

- Car payment & insurance: $450

- Gas: $150

- Phone (basic): $40

- Health insurance copays: $25

Wants ($1,749/month):

- Dining out: $400

- Streaming + subscriptions: $80

- Hobbies/entertainment: $300

- Shopping: $300

- Vacation savings: $300

- Misc lifestyle: $369

Savings & Debt ($1,166/month):

- 401(k) contribution: $600

- Roth IRA: $300

- High-yield savings (emergency fund): $266

That’s a fully functional middle-income household budget — and it builds nearly $14,000 a year in savings without feeling restrictive.

Does the 50/30/20 Rule Still Work in 2026?

Honestly? For most households, the rule needs adjusting. Here’s the truth based on current data:

In many US metros — San Francisco, New York, Boston, Seattle, San Diego, Miami — rent alone consumes 35–50% of take-home pay before any other expense. Harvard’s Joint Center for Housing Studies has shown that rents have outpaced incomes in most US counties since 2020. For households earning below the median income, basic needs frequently exceed 50% of take-home pay without any lifestyle excess.

This doesn’t mean the rule is broken. It means the percentages need to flex while the philosophy stays intact.

The core principles are still gold:

- Cap fixed essential costs so they don’t eat your life

- Build in guilt-free spending money so the system is sustainable

- Always pay yourself first — protect savings before lifestyle

What changes is the exact split.

Modified Versions of the 50/30/20 Rule

Depending on your situation, here are the realistic variations to consider:

The 60/20/20 Rule (High Cost of Living)

For people in expensive cities where housing alone takes 35%+ of income:

- 60% needs — accepts elevated housing costs as reality

- 20% wants — compressed lifestyle spending

- 20% savings — protected at all costs

The non-negotiable here is keeping savings at 20%. If you cut savings to make room for wants, the rule loses its long-term power.

The 70/20/10 Rule (Lower Income or Heavy Debt)

For households where essentials genuinely exceed 60% even after cutting:

- 70% needs — reality-check version

- 20% wants — kept intentionally to prevent burnout

- 10% savings — minimum viable savings

This is a transitional version. The goal is to increase income or reduce needs over 12–24 months to get back toward 50/30/20.

The 80/10/10 Rule (Aggressive Debt Payoff)

For people focused on eliminating high-interest debt:

- 80% needs + debt minimums + extra debt payments

- 10% wants

- 10% emergency fund only

Use this for 6–18 months until high-interest debt is eliminated, then return to 50/30/20.

The 50/30/20 Rule (Reversed — Aggressive Savers)

For higher earners or those chasing FIRE (Financial Independence, Retire Early):

- 50% savings & investments

- 30% needs

- 20% wants

This is rare but powerful — typically requires household income above $120,000 or living significantly below your means.

Step-by-Step: How to Start the 50/30/20 Budget This Week

You don’t need an app or a course. Here’s the entire setup in five steps:

Step 1: Calculate Your Take-Home Pay

Look at your last pay stub. The number you want is the amount that actually hits your bank account after taxes, health insurance, and 401(k) contributions are deducted. If you’re paid biweekly, multiply by 2.17 to get monthly take-home.

Step 2: Run the Math

Multiply your monthly take-home by 0.50, 0.30, and 0.20. Write the three numbers down. These are your monthly targets.

Step 3: Categorize Your Last 30 Days of Spending

Pull up your bank and credit card statements. Sort every transaction into Needs, Wants, or Savings. Add up the totals.

Step 4: Compare Reality to Target

This is where the truth comes out. Most first-time budgeters discover:

- Needs are higher than they thought (typically 55–65%)

- Wants are 2–3x higher than they realized

- Savings are near zero

Don’t panic. This is information, not failure.

Step 5: Adjust One Category at a Time

Don’t try to fix everything in week one. Pick the most impactful change:

- If wants is bloated → cancel 3 subscriptions today

- If needs is bloated → look at the “Big Three” (housing, transport, food)

- If savings is zero → automate $50/week into a high-yield savings account

Small consistent moves beat dramatic overhauls every time.

How to Automate the 50/30/20 Budget

Automation is what separates people who succeed at this rule from people who quit. Set up these three accounts:

- Primary checking — paycheck lands here, bills auto-pay from here (your 50% needs)

- Secondary checking or spending account — auto-transfer your 30% wants amount on payday

- High-yield savings account (HYSA) — auto-transfer your 20% on payday

When wants money runs out, you stop spending — without willpower. When savings auto-transfers, you save without thinking.

Top HYSA options in 2026 offer 4.00–4.75% APY, vs. 0.45% at traditional banks. On a $20,000 savings balance, that’s a $700–$800 annual difference for zero extra effort.

Common Mistakes Beginners Make

Mistake 1: Treating savings as the leftover. The whole point of the rule is to save first. If you wait until the end of the month, there’s never anything left.

Mistake 2: Misclassifying wants as needs. A car payment is a need; a $700/month luxury SUV payment when a $300/month sedan would work is mostly a want. Be honest about the line.

Mistake 3: Quitting after one bad month. If you spend 38% on wants in March, that’s not failure — that’s a data point. Adjust April and keep going.

Mistake 4: Ignoring annual or irregular expenses. Car registration, holiday gifts, summer travel — these blow up budgets when ignored. Build a small “sinking fund” inside savings to cover them.

Mistake 5: Using gross income instead of net. Always use take-home pay. Otherwise your math is off by 20–30% and your budget never balances.

Check our previous blog: How to Save $10,000 in 12 Months

Frequently Asked Questions

Is the 50/30/20 rule based on gross or net income?

The 50/30/20 budget rule is based on net income — your after-tax, take-home pay. This is the money that actually arrives in your bank account after federal tax, state tax, FICA, health insurance, and any pre-tax retirement contributions are deducted.

Where do retirement contributions fit in the 50/30/20 rule?

If your 401(k) contribution is pre-tax (deducted before your paycheck arrives), it’s already accounted for and doesn’t count again in your 20% savings bucket. If you contribute to a Roth 401(k), Roth IRA, or traditional IRA after receiving your paycheck, those contributions count toward your 20% savings.

What if my needs are more than 50% of my income?

This is the most common situation in 2026. You have three options: (1) reduce needs by cutting housing, transportation, or food costs (the “Big Three”), (2) increase income through a raise, side hustle, or career move, or (3) temporarily use a modified version like 60/20/20 or 70/20/10 while you work toward 50/30/20.

Is the 50/30/20 rule good for paying off debt?

It’s decent but not optimal for aggressive debt payoff. Minimum debt payments go in your 50% needs, and any extra payments go in your 20% savings & debt bucket. If you have high-interest credit card debt, consider temporarily using an 80/10/10 split to crush the debt faster, then return to 50/30/20.

How is the 50/30/20 rule different from zero-based budgeting?

The 50/30/20 rule uses three broad percentage buckets and requires minimal tracking. Zero-based budgeting assigns every single dollar a specific job before the month begins and requires detailed category tracking. The 50/30/20 method is better for beginners; zero-based budgeting offers more control for experienced budgeters.

Can I follow the 50/30/20 rule with irregular income?

Yes, but with modifications. Calculate your average monthly take-home from the last 6–12 months, then base your percentages on that. In high-income months, save the surplus; in low-income months, draw from that buffer. Freelancers and gig workers should aim for a 6-month emergency fund instead of 3 to absorb income volatility.

Final Thoughts

The 50/30/20 budget rule isn’t perfect, but it remains the best beginner framework in personal finance because it does three things almost no other system manages at once: it’s simple enough to remember, flexible enough to adapt, and balanced enough to sustain.

In 2026, the percentages may need to flex — 60/20/20 in expensive cities, 70/20/10 during tough seasons, 80/10/10 during aggressive debt payoff. But the underlying philosophy remains correct: protect savings, cap essentials, and leave room for joy.

Pick your numbers this week. Open the HYSA. Automate the transfers. Most people who try this for 90 days never go back to the chaos of unstructured spending — because once you’ve seen what intentional money management feels like, the old way feels like leaks in a bucket.

Your next paycheck is the starting line. Run the math today.